The Full Stack Economist is a newsletter for entrepreneurial economists who seek to manage a nation's economy from a holistic framework. It will report information and insights on all verticals necessary to running a healthy economy. In contrast to myopic theoretical economists, this publication will cater to practical economists interested in action. Borrowing from the software concept of the full stack developer — a developer that has mastered all major areas of coding — the full stack economist is an economist that has mastered all major areas of the economy. This newsletter is a product of Ryan Research.

Lesson of the Week:

What’s so special about manufacturing?

U.S. Manufacturing Sector - Innovation Frontier Project")

The Bloomberg podcast Odd Lots co-hosted by Joe Weisenthal and Tracy Alloway had a recent episode that featured guests David Oks and Henry Williams on development, industrialization, and globalization. At timestamp 6:58 Weisenthal asked, “what’s so special about manufacturing?” Willaims replied, “basically when you start manufacturing, you enter a process where long term your manufacturing productivity is going to converge with the global average and with the rest of the world. And so what that means is that manufacturing can really increase your national economic productivity. But in addition to that, it also absorbs a lot of surplus labor and it drives a broader process of economic complexification density and urbanization. That means that you get these economic cores that then create richer citizens.” This a fine answer to that question and both Williams and Oks go into further detail and nuance on the role of industrialization in development contrasting mainstream neoliberal economic narratives. I highly recommend giving it a listen.

Zooming out of that podcast, manufacturing must be seen as an imperative block of a full-stack economy. Erik S. Reinert is one of the most prominent economists that has articulated its importance. He precisely defines the reason for why manufacturing is so special: “the key mechanism to wealth is not manufacturing per se, but activities subject to increasing returns, technological change, and consequent dynamic imperfect competition under high barriers to entry…in industry: an increase in production would as a general rule have reduced costs. In manufacturing, the next machine one starts up will not be less effective than the previous one, rather the opposite; the next hour worked will reduce fixed costs per unit of production. In manufacturing, increasing production leads to falling unit costs. In manufacturing, increasing market share gives you the opportunity to get ahead in the race down the learning curve; in agriculture it drives you into the wall of diminishing returns…increasing returns means that as production expands – even without technical change – the cost of production per unit falls…the key to economic development was to have a large number of different economic activities, all subject to the falling costs of increasing returns…world prosperity requires that manufacturing industries and advanced service sectors are distributed to all nations.”

Reinert explained to us that manufacturing isn’t about making stuff for the sake of making stuff. It is about focusing on productive activities that have increasing returns to scale as in when you expand production, costs fall. This means your economy has more stuff that’s cheaper to buy. An economy that deepens into one activity while also spreading into other activities has a healthy recipe for growth. This virtuous cycle enables higher output, higher incomes, and a better quality of life for citizens. Think of it like a startup. A startup doesn’t grow by increasing the number of CEOs. It grows by hiring more and more employees with specialized skills in more and more categories such as accounting, marketing, sales, engineering, research, etc. Innovations can often come from the synergies produced between these fields such as a customer support department informing the engineering department of feedback or the sales department brainstorming with the marketing department. The growth and diversification of your staff inside your business is necessary for its revenue and profit growth. Most companies don’t decide to de-diversify their staffs once they reach a certain growth milestone and similarly, countries should not do that with their economies.

Reinert also contrasted manufacturing with traditional agriculture or commodity extraction activities because as you expand production of those activities, costs rise. Additionally, Reinert is wary of over-indulgence into a service economy because a healthy advanced service economy requires a manufacturing sector to sit on top of. Without such a relationship, a stand-alone service sector is not possible. For example, Reinert used Mongolia’s 1990s experience to demonstrate what shifting from an industrial economy to a high tech service economy guided by free market liberalism can do. Rather than making computer software like many Western economists thought, Mongolia’s free market economy destroyed industry and pushed people back into traditional diminishing returns activities like herding. “In only a few years, real wages had been almost halved and unemployment was rampant. The country’s imports exceeded the value of exports by a factor of two, and the real interest rate, corrected for inflation, was 35 per cent.” In the absence of manufacturing, Mongolians were forced into worse activities. These activities produced less and didn’t have the knowledge clusters necessary to move up the value chain. Thus, investment funds, consumer demand, and infrastructure were all well below what would be necessary to produce a sophisticated software sector. Reinert wrote, “this proves…it is better to have a relatively inefficient manufacturing sector than to have none at all.” The full-stack economy can be defined as the service sector stacked on top of the manufacturing sector stacked on top of the agricultural/commodity sector. You cannot have a secure and healthy economy if your country creates holes in that stack and relies on other countries to supply them.

News of the Week:

The Stanford AI Index Report: Measuring trends in Artificial Intelligence

“The AI Index is an independent initiative at the Stanford Institute for Human-Centered Artificial Intelligence (HAI), led by the AI Index Steering Committee, an interdisciplinary group of experts from across academia and industry. The annual report tracks, collates, distills, and visualizes data relating to artificial intelligence, enabling decision-makers to take meaningful action to advance AI responsibly and ethically with humans in mind.

Top 10 Takeaways:

Industry races ahead of academia

Perforamnce saturation on traditional benchmarks

AI is both helping an harming the environment

The world’s best new scientist…AI?

The number of incidents concerning the misuse of AI is rapidly rising.

The demand for AI-related professional skills is increasing across virtually every American industrial sector.

For the first time in the last decade, year-over-year private investment in AI decreased.

While the proportion of companies adopting AI has plateaued, the companies that have adopted AI continue to pull ahead.

Policymaker interest in AI is on the rise.

Chinese citizens are among those who feel the most positively about AI products and services. Americans… not so much.”

- AI Index Steering Committee, Institute for Human-Centered AI, Stanford University

The Age of Energy Insecurity: How the Fight for Resources Is Upending Geopolitics

“As recently as 18 months ago, many policymakers, academics, and pundits in the United States and Europe were waxing lyrical about the geopolitical benefits of the coming transition to cleaner, greener energy. They understood that the move away from a carbon-intensive energy system that relied on fossil fuels was going to be difficult for some countries. But on the whole, the conventional wisdom held that the shift to new sources of energy would not only aid the fight against climate change but also put an end to the troublesome geopolitics of the old energy order. Such hopes, however, were based on an illusion. The transition to clean energy was bound to be chaotic in practice, producing new conflicts and risks in the short term. By the fall of 2021, amid an energy crisis in Europe, skyrocketing natural gas prices, and rising oil prices, even the most optimistic evangelist of the new energy order had realized that the transition would be rocky at best. Any remaining romanticism evaporated when Russia invaded Ukraine in February 2022. The war revealed not only the brutal character of Russian President Vladimir Putin’s regime and the dangers of an excessive energy dependence on aggressive autocracies but also the risks posed by a jagged, largely uncoordinated scramble to develop new energy sources and to wean the world off old, entrenched ones.”

- Jason Bordoff and Meghan L. O’Sullivan at Foreign Affairs

The Gigantic Austerity Drive Underway

“We are quietly witnessing the largest shift to austerity undertaken in this century. Debt-strained developing countries are making further cuts to already ragged budgets, in many cases as they battle to meet punishing new conditions demanded by the International Monetary Fund (IMF), which held its Spring Meetings last week in Washington DC.”

- Kate Mackenzie and Tim Sahay at The Polycrisis

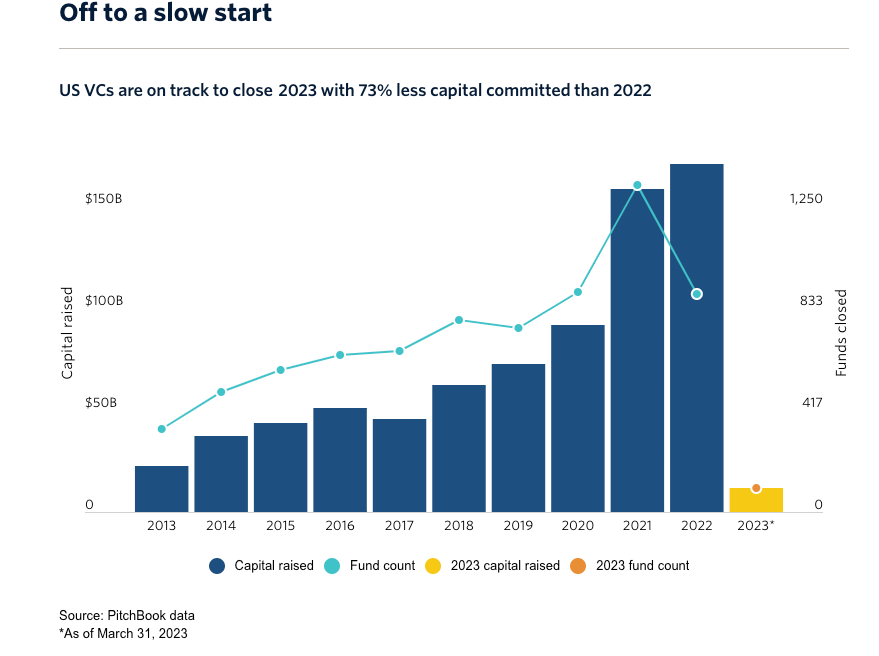

VC fundraising screeches to a halt in Q1

“The fallout from the startup industry's exit slowdown continued into Q1, and managers attempting to secure capital commitments for new funds are still feeling the burn. Exits dropped off a cliff in mid-2022 and have failed to pick back up, leaving gobs of LP capital tied up in late-stage unicorns. US VC firms raised $11.7 billion across 99 funds in Q1, according to a first look at the latest PitchBook-NVCA Venture Monitor. If that fundraising pace were to continue through the rest of the year, it would mean the lowest total capital raised since 2017 and a 73% drop relative to 2022.”

- Rosie Bradbury at Pitchbook

Lithium manufacturing: demand for EVs outstrips supply

“Without batteries, the vision for electric vehicles (EVs) is null and void. But, the industry is putting a higher demand on lithium—the primary component of conventional batteries—that must be actioned to fulfil the needs of automotive expansion. According to the World Economic Forum, each individual EV battery requires around eight kilograms of lithium. Other data suggests that around 100,000 metric tonnes of lithium is produced by the global mining industry, which, if supplied purely to the EV sector, would be enough to manufacture batteries for 12,500,000 EVs each year. Sadly this can’t be achieved, especially if electrification is to increase its digital footprint. More devices means more batteries, so how can businesses make more lithium?”

- Tom Swallow at Manufacturing Digital

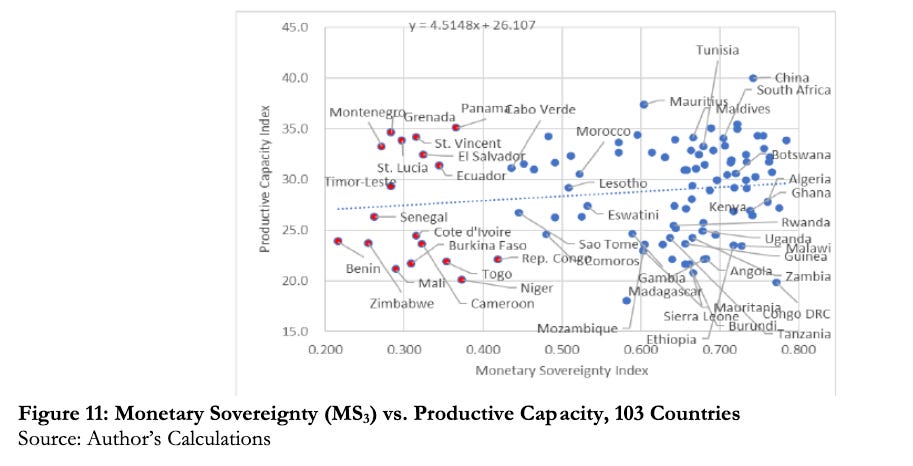

Decolonization 2.0: Realizing Africa's Promise through Economic Sovereignty and Strategic Finance

“This paper explains this puzzle by the fact that, while many African countries achieved political independence in the second half of the 20th century through the process of decolonization, most remain economically, and especially monetarily, dependent on developed economies, multinational corporations and international financial institutions. Different development models in the past four decades have not been able to transform these countries to a successful path of sustainable development due to their undue reliance on foreign finance based on a misunderstanding of the geopolitical nature of money and finance. Instead we build on the historical reality that all money is a liability of the state (and a credit of its holder) rather than a private commodity, implying that finance is credit creation (not intermediation). As such, development at the national level is not about getting more money but building productive capacity. However, countries that do not issue their own currency, or rely extensively on foreign debt and imports have reduced monetary sovereignty. We construct three iterations of a Monetary Sovereignty Index and compare countries’ scores on it with their productive capacity.”

- Jacob Assa

Mercantilist Deals of the Great Powers

“Each of these diplomatic journeys are the result of growing preoccupations with industrial policy, fragmentation, and the energy transition thanks to tensions around China and Russia. Trade flows, supply chains, and entire industries are rapidly being reorganized. Free trade led by “cooperative factions” in key countries has given way to “friend-shoring” led by “restrictionist” factions, largely on grounds of national security. New policies on export controls, visa bans, investment blocks, and sanctions are redirecting the flow of goods and people. US Allies, adversaries, and firms face hard questions: Who can invest in your country? Who can you sell to? What can and can’t you sell? Which countries do you risk arrest for trading with?”

- Kate Mackenzie and Tim Sahay at The Polycrisis

Lessons from Denmark's thriving district heating sector

“District heating accounts for 10 per cent of the heat supply in the European Union, yet the concept is still strange to many across the region. Instead of distributing gas to individual household boilers, district heating or heat networks take the heat from a centralised location and transport it through insulated pipes to homes and businesses. In Denmark, a global forerunner in this technology, most people are familiar with it, and the municipality of Nyborg is a good example: 65 per cent of its 32,000 inhabitants have access to the district heating system run by the local utility company, Nyborg Forsyning & Service.”

- The Engineer

Get Ready for Lower Fuel Prices — and Slower Inflation

“Oil is the world’s foremost commodity. Nations fight wars to control it; economies wax and wane based on its price. But oil is also useless without a process to transform it into the stuff everyone needs: gasoline, diesel, jet fuel and petrochemicals. Over the last couple of years, the refining industry became a chokepoint, pushing the cost of turning crude into fuels to an all-time high, in turn inflating gasoline and diesel prices. The “refinery wall” was the buzzword. Now, the bottleneck is easing.”

- Javier Blas at Bloomberg

The India Stack: opening the digital marketplace to the masses

“At the heart of this effort is the so-called India Stack: government-backed APIs, or application programming interfaces, upon which third parties can build software with access to government IDs, payment networks and data. This digital infrastructure is interoperable and “stacked” together — meaning that private companies can build apps integrated with state services to provide consumers with seamless access to everything from welfare payments to loan applications. Supporters argue that India has found a world-beating solution for building out and regulating the online commons that is more equitable than the US’s laissez-faire approach, more innovative than the EU’s regulation-heavy model and more transparent than China’s totalitarian template. Now, as New Delhi hosts this year’s G20 presidency and surpasses China as the world’s most populous country, India’s public digital infrastructure has become a core part of Prime Minister Narendra Modi’s efforts to present India as a nascent economic superpower, alternative investment destination to China and leading voice of the global south.”

- Benjamin Parkin, John Reed, and Jyotsna Singh at Financial Times

Does Europe need to split?

“Emmanuel Macron’s call for Europe to reduce its dependency on the United States and develop its own “strategic autonomy” caused a transatlantic tantrum. The Atlanticist establishment, in the US as much as in Europe, responded in a typically unrestrained fashion — and, in doing so, missed something crucial: Macron’s words revealed less about the state of Euro-American relations than they did about intra-European relations. Very simply, the “Europe” Macron speaks of no longer exists, if it ever did. On paper, almost the entire continent is united under one supranational flag — that of the European Union. But that is more fractured than ever. On top of the economic and cultural divides that have always plagued the bloc, the war in Ukraine has caused a massive fault line to re-emerge along the borders of the Iron Curtain. The East-West divide is back with a vengeance.”

- Thomas Fazi at UnHerd

Germany Draws Up €2 Billion State Fund to Secure Key Commodities

“The German government plans to set up a state fund worth up to €2 billion ($2.2 billion) that will support mining of raw materials critical to the nation’s green transition, with the aim of securing access and cutting reliance on China. The new financing vehicle could start next year if the ruling coalition agrees on the funding, according to people familiar with the matter, and will be equipped with funds between €1 billion and €2 billion. The pivotal role of raw materials such as cobalt, copper, lithium, silicon and rare earth metals in producing everything from wind turbines to electric-vehicle batteries is driving efforts to guarantee supplies across the globe. Germany relies on imports for over 90% of crucial commodities, according to research by think tank DIW Berlin, with China leading the the way in supplying many important inputs.”

- Kamil Kowalcze and Michael Nienaber at Bloomberg

A Free Republic Depends on Worker Power

“Despite their disagreements, what republicans from Thomas Jefferson and Hamilton to Lincoln and Frederick Douglass recognized, and what many current members of the Republican Party appear to miss, is the link between economic power and opportunity and that virtue. It makes no sense, for example, to implore workers to be more industrious and take greater personal responsibility while adopting policies that lead to declining or stagnating wages and diminish worker power and security in the marketplace. One crucial source of virtue is the hope that through hard work they can achieve a better life for themselves and their communities. If Americans want more virtuous workers and citizens, we need to restore that hope through more worker-friendly policies.”

- Joshua Preiss at The American System

Could an acceleration in digital transformation be the one upside of the energy cost crisis?

“The current energy crisis is therefore an opportunity to show SME manufacturers the possibilities and benefits of digital adoption, through a lens that is meaningful. It is an immediate and tangible challenge that almost all SME manufacturers are facing, which can be addressed quickly. If experts and technology providers seize this opportunity, digital transformation can be boosted to help lower operational costs, while driving forward sophistication and innovation in our manufacturing supply chain. One clear pathway to how this can be achieved within SME manufacturers is through energy optimisation. Reviewing present schedules, equipment and processes to ensure they are being utilised in a way that optimises energy usage, can be a low-cost solution to how SME manufacturers can combat rising energy costs.”

- Craig Beck at The Manufacturer