Irish Banks Are Starving Ireland’s Economy

In 1922, Michael Collins wrote “Business cannot succeed without capital. Millions of Irish money are lying idle in banks.” He referred to the fact that while honest and hard-working Irish people responsibly accumulated savings, the Irish banks neglected their duty to finance domestic Irish business at an appropriate level justified by the savings available. Over 100 years later, Ireland appears to be in a similar situation.

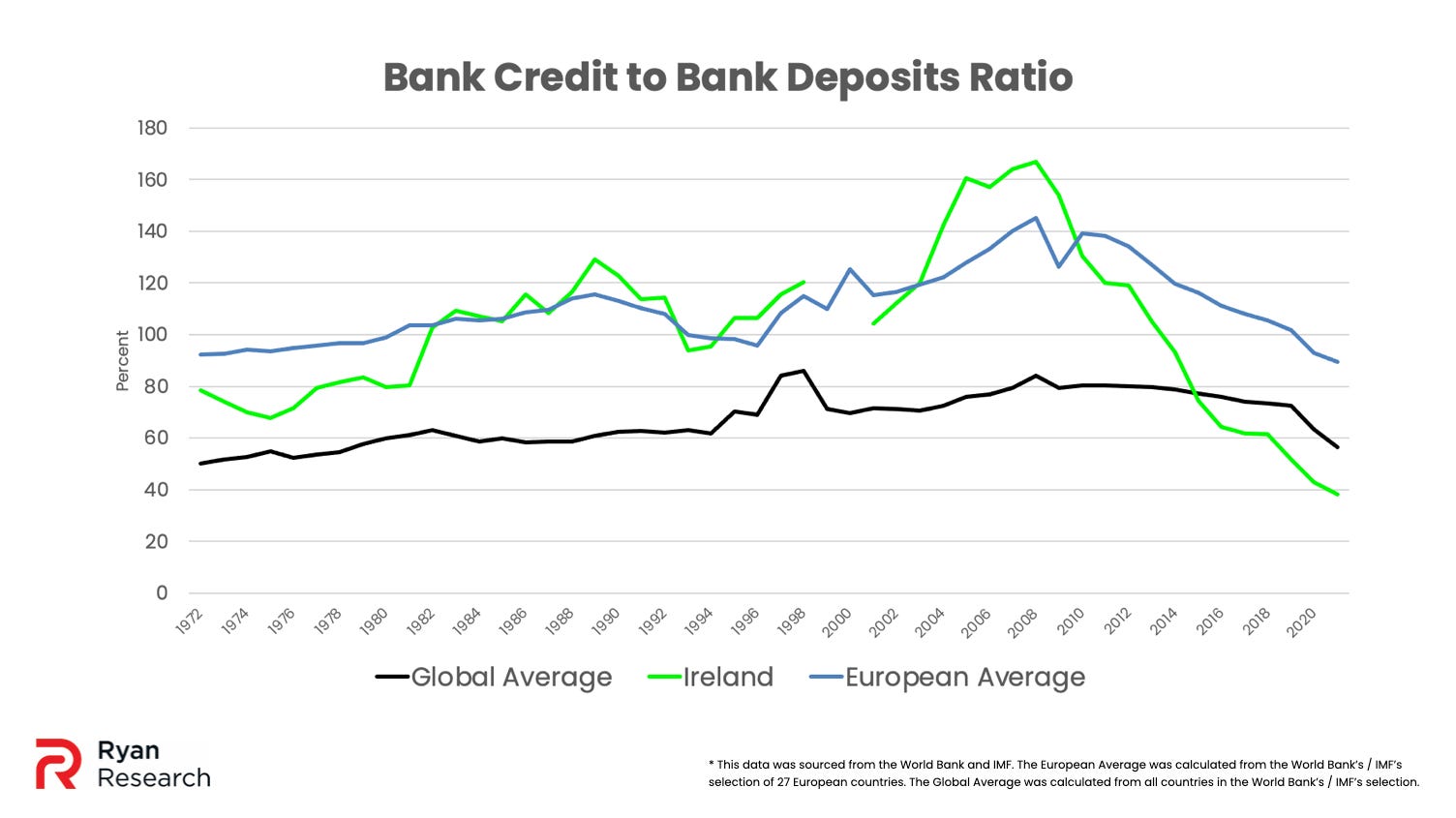

The bank credit to bank deposit ratio is defined as the total of all loans given out by banks divided by the total customer deposits at banks. Common sense and economic logic suggest that banks should have adequate deposits to back up their loans. A ratio over 100 percent indicates more credit than deposits, while one below 100 percent indicates more deposits than credit.

While it’s easy to see how credit could be expanded too much relative to deposits, too little credit relative to deposits can also spell problems. The following data was collected from the U.S. Federal Reserve, the International Monetary Fund (IMF), the World Bank, and the Irish Central Statistics Office (CSO).

Ireland’s bank credit to bank deposit ratio was 38 percent as of 2021. The ratio declined by 77 percent from its 2008 high of 167 percent. While some diminishment might be expected from that period, it has severely gone below an appropriate level. From 1972, the ratio declined by 52 percent. From 1960, the ratio declined by 38 percent. How is it possible that present-day Ireland requires substantially less credit relative to deposits than 50 to 60 years ago? This is absurd on its face. Ireland’s 2021 bank credit to bank deposit ratio was 57 percent below the European average. For example, it was 57 percent lower than Germany’s, 59 percent lower than the Netherlands’, 65 percent lower than France’s, 75 percent lower than Sweden’s, 78 percent lower than Norway’s, and 86 percent lower than Denmark’s. Ireland has the second lowest recorded ratio in Europe.

Finally, Ireland’s ratio is 32 percent lower than the global average, and is, in fact, one of the lowest recorded in the world. Angola followed by Zambia sat lower than Ireland followed by Ghana then Sudan which sat higher.

The bottom-line here is that Irish banks are not lending as much as they should be. They are well below the healthy level of lending let alone a level that would cause concern. When banks lend more it allows businesses to invest in order to innovate and expand their operations stimulating economic growth and job creation. On the consumer side, increased credit provides needed financing and expands demand for goods and services from the business sector.

Specific sectors are more reliant on bank credit than others. Construction is one such business sector. A 2017 report from the Construction Industry Federation showed that construction companies were “experiencing difficulty in securing finance” with “many companies reporting that they are unable to access finance from external sources and are dependent on dwindling cash reserves.”

As the CIF pointed out “these are the companies the Government is dependent on to resolve the housing crisis and deliver Ireland’s infrastructure. They cannot do so without access to finance.”

It is probable to estimate that Ireland’s current housing shortage could be partly ameliorated if Irish banks increased their lending. As noted in a previous Gript article by the author, the total nominal value of Irish bank lending to the construction sector is at extreme lows. For perspective, the nominal levels of credit in the U.S. and Euro Area have substantially increased since the conclusion of the 2008 financial crisis while the levels in Ireland have substantially decreased.

Ireland should research and debate policy solutions that would increase the bank credit to bank deposit ratio through the expansion of bank credit. It must be noted that foreign financial firms have filled some of the credit gap in Ireland.

However, foreign lenders will have different incentives, priorities, and strategies than domestic lenders. Domestic lenders will have more rootedness in local areas which helps grow small to medium sized enterprises and provide financing for ordinary citizens. Foreign lenders will be less concerned with those matters and seek out unholistic lending in things like luxury condo development.

These investment funds are buying up large swathes of Irish new builds to rent, out-bidding Irish families and pushing rents up higher. Foreshadowing this activity, Collins cautioned that “investors and exploiters from outside will come in to reap the rich profits…they will bring with them all the evils that we want to avoid in the new Ireland.” Perhaps Ireland should listen to him there as well as on the general advocacy to expand domestic bank lending because it has the savings to justify it.

Originally published on Gript on 27/08/2024:

https://gript.ie/irish-banks-are-starving-irelands-economy/